Financial market data - yield curve - Published series

Data - ECB

Info

Data on monetary policy

| source | dataset | Title | .html | .rData |

|---|---|---|---|---|

| bdf | FM | Marché financier, taux | 2026-07-24 | 2026-07-24 |

| bdf | MIR | Taux d'intérêt - Zone euro | 2026-07-24 | 2026-07-24 |

| bdf | MIR1 | Taux d'intérêt - France | 2026-07-24 | 2026-07-24 |

| bis | CBPOL | Policy Rates, Daily | 2026-07-25 | 2026-07-25 |

| ecb | BSI | Balance Sheet Items | 2026-07-24 | 2026-07-23 |

| ecb | BSI_PUB | Balance Sheet Items - Published series | 2026-07-24 | 2026-07-24 |

| ecb | FM | Financial market data | 2026-07-24 | 2026-07-24 |

| ecb | ILM | Internal Liquidity Management | 2026-07-24 | 2026-07-24 |

| ecb | ILM_PUB | Internal Liquidity Management - Published series | 2026-07-24 | 2026-07-24 |

| ecb | MIR | MFI Interest Rate Statistics | 2026-07-24 | 2026-07-24 |

| ecb | RAI | Risk Assessment Indicators | 2026-07-24 | 2026-07-24 |

| ecb | SUP | Supervisory Banking Statistics | 2026-07-24 | 2026-07-24 |

| ecb | YC | Financial market data - yield curve | 2026-07-24 | 2026-07-23 |

| ecb | YC_PUB | Financial market data - yield curve - Published series | 2026-07-24 | 2026-07-24 |

| ecb | liq_daily | Daily Liquidity | 2026-07-24 | 2026-07-24 |

| eurostat | ei_mfir_m | Interest rates - monthly data | 2026-07-23 | 2026-07-23 |

| eurostat | irt_st_m | Money market interest rates - monthly data | 2026-07-24 | 2026-07-23 |

| fred | r | Interest Rates | 2026-07-24 | 2026-07-24 |

| oecd | MEI | Main Economic Indicators | 2026-07-24 | 2025-07-24 |

| oecd | MEI_FIN | Monthly Monetary and Financial Statistics (MEI) | 2024-09-15 | 2025-07-24 |

Data on interest rates

| source | dataset | Title | .html | .rData |

|---|---|---|---|---|

| bdf | FM | Marché financier, taux | 2026-07-24 | 2026-07-24 |

| bdf | MIR | Taux d'intérêt - Zone euro | 2026-07-24 | 2026-07-24 |

| bdf | MIR1 | Taux d'intérêt - France | 2026-07-24 | 2026-07-24 |

| bis | CBPOL_D | Policy Rates, Daily | 2026-07-25 | 2025-08-20 |

| bis | CBPOL_M | Policy Rates, Monthly | 2026-07-25 | 2026-07-25 |

| ecb | FM | Financial market data | 2026-07-24 | 2026-07-24 |

| ecb | MIR | MFI Interest Rate Statistics | 2026-07-24 | 2026-07-24 |

| eurostat | ei_mfir_m | Interest rates - monthly data | 2026-07-23 | 2026-07-23 |

| eurostat | irt_lt_mcby_d | EMU convergence criterion series - daily data | 2026-07-24 | 2025-07-24 |

| eurostat | irt_st_m | Money market interest rates - monthly data | 2026-07-24 | 2026-07-23 |

| fred | r | Interest Rates | 2026-07-24 | 2026-07-24 |

| oecd | MEI | Main Economic Indicators | 2026-07-24 | 2025-07-24 |

| oecd | MEI_FIN | Monthly Monetary and Financial Statistics (MEI) | 2024-09-15 | 2025-07-24 |

| wdi | FR.INR.DPST | Deposit interest rate (%) | 2026-07-25 | 2026-07-24 |

| wdi | FR.INR.LEND | Lending interest rate (%) | 2026-07-25 | 2026-07-24 |

| wdi | FR.INR.RINR | Real interest rate (%) | 2026-07-25 | 2026-07-24 |

Last

| TIME_PERIOD | FREQ | Nobs |

|---|---|---|

| 2026-07-23 | B | 10 |

TITLE

Code

YC_PUB %>%

group_by(TITLE) %>%

summarise(Nobs = n()) %>%

arrange(-Nobs) %>%

print_table_conditional| TITLE | Nobs |

|---|---|

| AAA yield curve - 1-year instantaneous forward rate | 5593 |

| AAA yield curve - 1-year spot rate | 5593 |

| AAA yield curve - 10-year instantaneous forward rate | 5593 |

| AAA yield curve - 10-year spot rate | 5593 |

| AAA yield curve - 2-year instantaneous forward rate | 5593 |

| AAA yield curve - 2-year spot rate | 5593 |

| AAA yield curve - 3-month spot rate | 5593 |

| AAA yield curve - 5-year instantaneous forward rate | 5593 |

| AAA yield curve - 5-year spot rate | 5593 |

| AAA yield curve - spread between 10-year and 1-year spot rates | 5593 |

INSTRUMENT_FM

Code

YC_PUB %>%

left_join(INSTRUMENT_FM, by = "INSTRUMENT_FM") %>%

group_by(INSTRUMENT_FM, Instrument_fm) %>%

summarise(Nobs = n()) %>%

arrange(-Nobs) %>%

print_table_conditional| INSTRUMENT_FM | Instrument_fm | Nobs |

|---|---|---|

| G_N_A | Government bond, nominal, all issuers whose rating is triple A | 55930 |

DATA_TYPE_FM

Code

YC_PUB %>%

left_join(DATA_TYPE_FM, by = "DATA_TYPE_FM") %>%

group_by(DATA_TYPE_FM, Data_type_fm) %>%

summarise(Nobs = n()) %>%

arrange(-Nobs) %>%

print_table_conditional| DATA_TYPE_FM | Data_type_fm | Nobs |

|---|---|---|

| IF_10Y | Yield curve instantaneous forward rate, 10-year maturity | 5593 |

| IF_1Y | Yield curve instantaneous forward rate, 1-year maturity | 5593 |

| IF_2Y | Yield curve instantaneous forward rate, 2-year maturity | 5593 |

| IF_5Y | Yield curve instantaneous forward rate, 5-year maturity | 5593 |

| SRS_10Y_1Y | Yield curve spot rate, spread between the 10-year and 1-year maturity | 5593 |

| SR_10Y | Yield curve spot rate, 10-year maturity | 5593 |

| SR_1Y | Yield curve spot rate, 1-year maturity | 5593 |

| SR_2Y | Yield curve spot rate, 2-year maturity | 5593 |

| SR_3M | Yield curve spot rate, 3-month maturity | 5593 |

| SR_5Y | Yield curve spot rate, 5-year maturity | 5593 |

TIME_PERIOD

Code

YC_PUB %>%

group_by(TIME_PERIOD) %>%

summarise(Nobs = n()) %>%

arrange(desc(TIME_PERIOD)) %>%

print_table_conditional()Government bond, nominal, all issuers whose rating is triple A

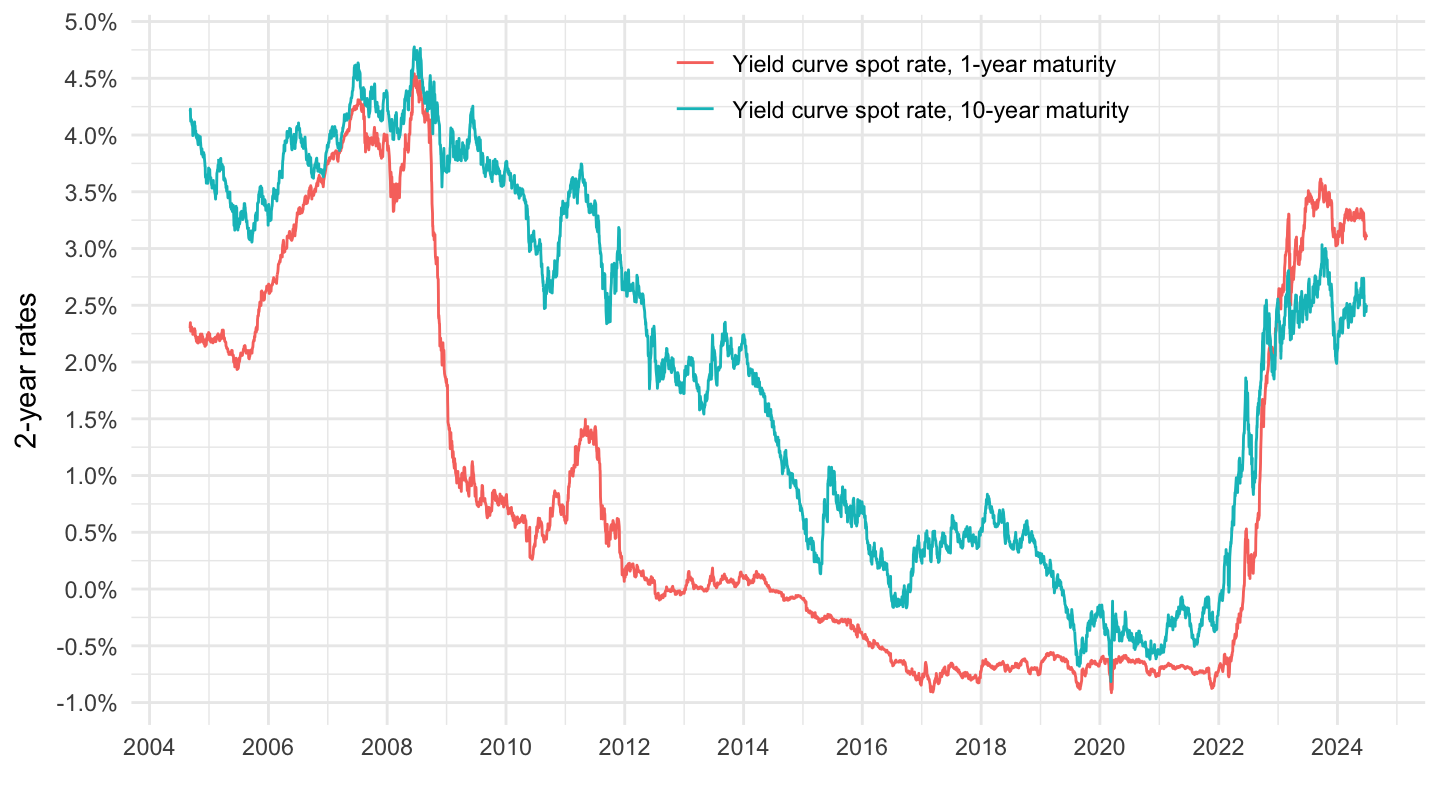

1 year, 10 year

Code

YC_PUB %>%

filter(DATA_TYPE_FM %in% c("SR_10Y", "SR_1Y")) %>%

select_if(~ n_distinct(.) > 1) %>%

rename(date = TIME_PERIOD) %>%

arrange(desc(date)) %>%

left_join(DATA_TYPE_FM, by = "DATA_TYPE_FM") %>%

ggplot + geom_line(aes(x = date, y = OBS_VALUE/100, color = Data_type_fm)) +

theme_minimal() + xlab("") + ylab("Interest rates") +

scale_x_date(breaks = seq(1960, 2100, 2) %>% paste0("-01-01") %>% as.Date,

labels = date_format("%Y")) +

scale_y_continuous(breaks = 0.01*seq(-10, 50, 0.5),

labels = percent_format(accuracy = .1)) +

theme(legend.position = c(0.6, 0.9),

legend.title = element_blank())

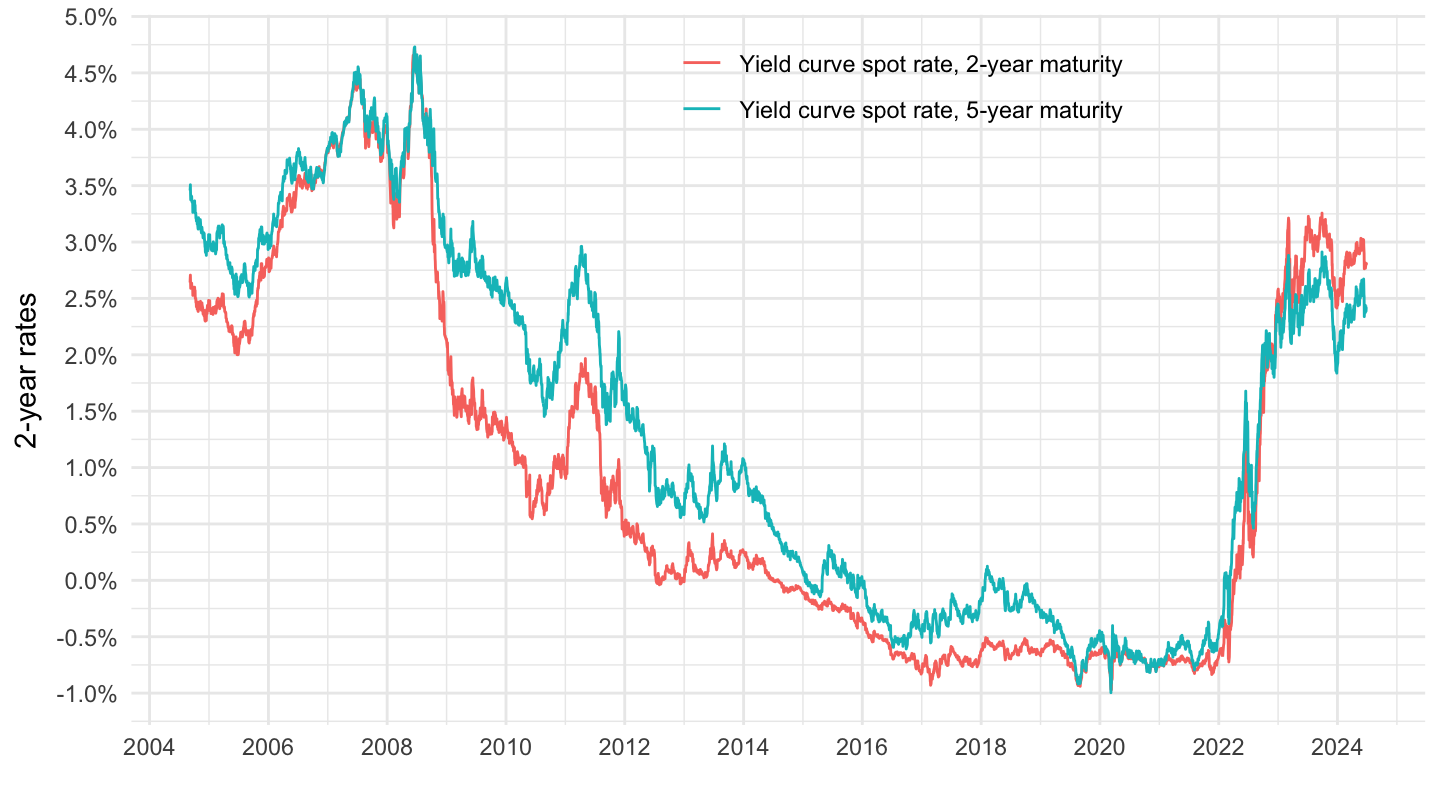

2 years, 5 years, 7 years

Code

YC_PUB %>%

filter(DATA_TYPE_FM %in% c("SR_2Y", "SR_5Y", "SR_7Y")) %>%

select_if(~ n_distinct(.) > 1) %>%

rename(date = TIME_PERIOD) %>%

arrange(desc(date)) %>%

left_join(DATA_TYPE_FM, by = "DATA_TYPE_FM") %>%

ggplot + geom_line(aes(x = date, y = OBS_VALUE/100, color = Data_type_fm)) +

theme_minimal() + xlab("") + ylab("2-year rates") +

scale_x_date(breaks = seq(1960, 2100, 2) %>% paste0("-01-01") %>% as.Date,

labels = date_format("%Y")) +

scale_y_continuous(breaks = 0.01*seq(-10, 50, 0.5),

labels = percent_format(accuracy = .1)) +

theme(legend.position = c(0.6, 0.9),

legend.title = element_blank())