Inflation and purchasing power: It’s the politics, stupid!

[🌐 HTML Presentation] [🎞️ PDF Presentation] [📄 PDF Article]

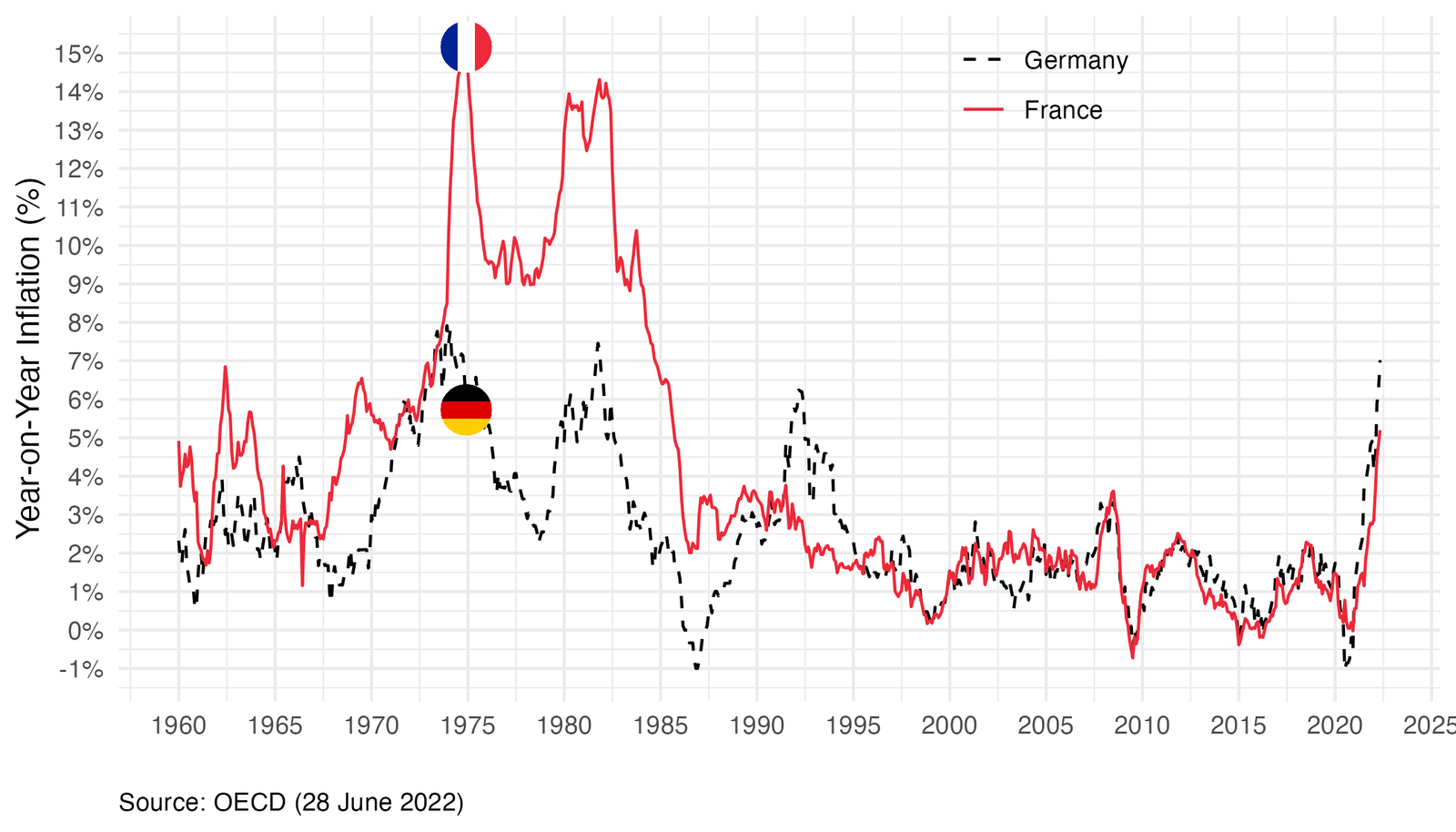

Since the reopening of the economy following the COVID-19 crisis, and the war in Ukraine, advanced economies have been facing a surge in inflation not seen since the 1970s or 1980s. In France, in June 2022, year-on-year inflation stood at 5.8% according to the Consumer Price Index (6.5% according to the Harmonised Index at the European level, which is more representative of actual inflation as it excludes reimbursed healthcare expenditures), and is expected to reach 6.5–7% by the end of the year according to INSEE’s latest economic outlook note of June 24, 2022 (Insee 2022)1. Figure Figure 1 shows that, despite the acceleration in inflation since the beginning of 2021, France is still far from the inflationary dynamics of the 1970s. In Europe as well as in the United States, this resurgence of inflation has raised concerns about purchasing power, which have come to dominate both the political and media agenda. In France, by the end of June 2022, there were plans to quickly present a bill to the Council of Ministers introducing several emergency measures. Numerous policies aimed at supporting household purchasing power have been announced by public authorities: energy price caps, pension increases, the unfreezing of the public sector wage index point, caps on rent increases, and so on.

In this text, we take a step back to clarify the link between inflation and purchasing power, and to put the economic debates surrounding inflation into perspective. One of our main messages is that understanding the relationship between inflation and purchasing power requires approaches and data beyond those currently available, and that the appropriate response - far from any single economic doctrine on how to address inflation - ultimately involves a political debate over how the burden is shared across different groups of people or sectors. It is therefore a political debate that cannot be reduced to technical disputes.

Inflation or relative price movements?

Strictly speaking, the term “inflation” should be reserved for situations involving a generalized increase in both prices and wages—something observed notably in the 1970s or during episodes of hyperinflation. However, this is not what is currently being observed in France, where some prices are indeed rising, but not all, and where some wages are also increasing, though not to the same extent. What we are experiencing, therefore, is not “inflation” in the strict sense of a general rise in prices and wages, but rather increases in certain prices and the associated loss of purchasing power, as most incomes do not keep pace with these changes.

From a purely accounting perspective, one may ask what share of inflation directly results from increases in oil prices and commodity prices (potentially compounded, in Europe’s case, by exchange rate depreciation, given that oil prices are denominated in dollars), and what share stems from the direct and indirect effects of these increases in energy and food prices. Core inflation—which excludes the direct impact of energy and food prices on the price index—stood at 3.7% in May 2022, indicating that observed inflation is not limited to these two components. However, energy has far-reaching effects: for example, rising oil prices almost mechanically lead to higher airline ticket prices due to increased kerosene costs, which are included in core inflation. Many other industries consume energy and agricultural products, either directly or indirectly. Moreover, inflation is also mechanically amplified through various indexation mechanisms: for instance, the rent reference index (IRL) is directly linked (with a lag) to inflation excluding rents and tobacco, which explains the transmission of energy prices to rents. The revaluation of the minimum wage (SMIC), which also depends on inflation, in turn affects service prices—for example, in the hospitality sector. These price increases then feed back into further increases in rents and the minimum wage. Overall, increases in oil and food prices alone can lead to a significant rise in core inflation.

Beyond the impact of relative price movements on households’ real incomes, there is also an aggregate loss of purchasing power for France. As in the 1970s, inflation originates in rising prices of commodities that the country does not produce and is primarily driven by higher prices of imported goods. This corresponds to a loss of purchasing power insofar as one seeks to avoid the external indebtedness that would otherwise result from this additional burden. From this perspective, and in terms of aggregate purchasing power, one may question whether inflation itself is truly the problem, or rather the external transfer associated with it.

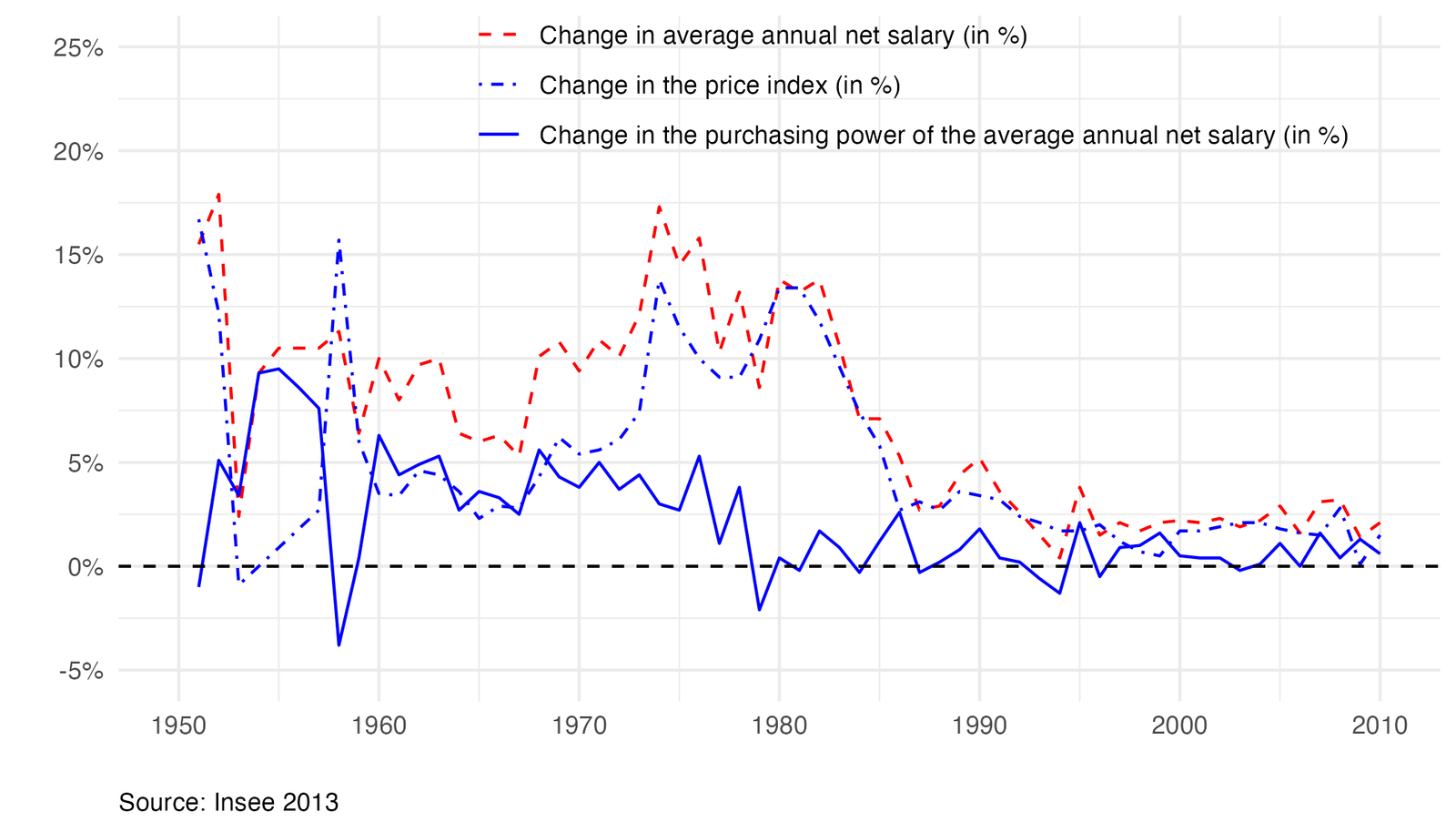

Inflationary episodes have not always been accompanied by a decline in purchasing power (Figure 2), because incomes have often increased at the same pace—or even faster—than inflation, due to market dynamics, discretionary public policies, or indexation mechanisms. For example, in France in the late 1960s and early 1970s, inflation was relatively high (around 5%, see Figure 2), but net wages were rising even faster (around 10% per year), so inflation was not perceived negatively: the purchasing power of the average annual net wage was increasing by about 5%. Since the period of high inflation combined with low economic growth in the 1970s (“stagflation”), it has become customary to associate inflation with a loss of purchasing power, but this direction of causality is far from obvious in general. The idea that low inflation (or, equivalently, a strong currency) is preferable to higher inflation is not self-evident, either theoretically or historically. Yet it has become a widely held belief, likely stemming from the inflationary excesses of the 1970s and 1980s, the debates over the “strong franc” policy in the 1980s and 1990s, and the fact that institutions of the Eurozone—particularly the European Central Bank—tend to equate fighting inflation with protecting purchasing power. This is all the more understandable given that inflation (an increase in the price of goods and services expressed in monetary units) is equivalent to a loss of the purchasing power of money in terms of those goods and services.

Moderately high inflation that is not accompanied by a decline in purchasing power does not have only drawbacks. Before the inflationary episode that began in 2021–2022, it was common to complain about inflation being too low, as it had remained persistently below 2%. For those who view public debt as a problem, inflation allows for a reduction in public debt without austerity; more generally, it benefits borrowers and disadvantages creditors—provided the latter are not protected by indexation clauses. Moreover, moderate inflation can help grease the wheels of economic and social transformation: downward wage rigidity makes intersectoral adjustments difficult, and within firms it complicates differentiated wage-setting—for example, in favor of new entrants. Overall, inflation can help erode rents and entrenched positions.

That said, the costs of inflation typically highlighted to justify central banks’ mandates appear limited. In the New Keynesian models commonly used by central banks, the standard argument is that excessive inflation leads to significant price dispersion and disrupts the pricing system. Yet even during the high-inflation period of the 1970s–80s, these costs seemed relatively modest (Nakamura et al. 2018). The current anti-inflation consensus is therefore not easily explained. Should it also be seen as a way of protecting creditors, pensions, and rents? Or perhaps as the work of “fear merchants,” who stigmatize any signal from the economic outlook as a new source of anxiety, thereby filling the media space and public debate while responding to a collective need for a dominant concern? Our skepticism, however, does not concern the need to pay attention to inflation dynamics, but rather the tendency to focus, at a given moment, on a single—imperfect and partial—indicator as representative of an economy’s or society’s problems, and to frame all other issues in relation to it.

What are the causes of inflation?

Economists have not developed a consensus view of inflation in general, and even less so of the current episode. It can be attributed to several causes: a chaotic restart of the economy after the COVID-19 pandemic (historically, post-crisis or post-war periods are often conducive to inflation, as value chains are disrupted), the war in Ukraine, renewed lockdowns in China linked to its “zero-COVID” policy, or the monetary and fiscal policies implemented before the pandemic or even since 2008, among others.

Because there is no consensus on the causes of inflation, it is tempting for each observer to project their own interpretations onto the issue. In France, some see current inflation as the bill for the “whatever it takes” policy—a way of paying for past excesses, both fiscal and monetary. This view is shared by observers with otherwise very different perspectives. Some economists have, since 2008, criticized the massive liquidity injections by central banks and governments, regularly predicting that they would soon lead to runaway inflation. Others, often described as more “progressive,” also interpret current inflation as evidence of the limits of financing public spending through debt rather than through higher taxation of the wealthy, calling for instance for the return of a wealth tax (ISF) (Piketty 2022). For them, the “whatever it takes” must ultimately be paid for one way or another, and to avoid this burden falling on lower-income households (through inflation), it should instead fall on the wealthiest.

New Keynesian economists typically analyze inflation through the lens of the Phillips curve: within this framework, inflation reflects an excessively low level of unemployment, itself the result of overly expansionary macroeconomic policies—i.e., an “overheating” economy. This theory implies that inflation is primarily wage-driven (that is, triggered by an initial increase in nominal wages), which then feeds into production costs and thus into prices. However, this mechanism—where wage inflation translates into price inflation—was not observed during the 2021–2022 inflationary episode, not even in the United States, where macroeconomic policy had been the most expansionary: prices rose before wages, and by more.

One can also look beyond national borders to understand what drives inflation. At the European level, inflation is primarily shaped by dependence on energy and food prices, which themselves depend on the energy mix and agricultural production, but also on the extent to which increases in these prices are passed through to consumers. For energy prices, this depends, for example, on the role of regulated tariffs for gas and electricity, and on the share of consumers on variable-price contracts. At an aggregate level, the loss of purchasing power induced by rising energy prices depends not only on the national energy mix, but also on the extent to which producers and distributors of gas, electricity, and oil hedge against price fluctuations. As a result, the true magnitude of the increase in the energy bill is itself difficult to assess (Geerolf et al. 2022).

Demand shock or supply shock: how should we respond?

As with the stagflation of the 1970s, the current macroeconomic situation challenges standard aggregate macroeconomic models. Rising oil prices are often described in these models (such as the so-called AS/AD model—aggregate supply/aggregate demand) as a “supply shock,” meant to explain the simultaneous emergence of inflation and unemployment, since price increases cannot be fully passed on to consumers, implying a decline in profit margins, firms’ investment capacity, and so on. However, this distinction between a supply shock and a demand shock is not entirely convincing here: isn’t an increase in the price of oil, gas, or other commodities also a demand shock—or both at once—inasmuch as it reduces disposable income after essential expenditures on energy and food, and therefore lowers consumption? Moreover, as in the 1970s, there is no real recycling of “petrodollars,” so rising energy prices may further increase the global excess of savings, as well as inequalities in its distribution across countries: inflation is not “lost” for everyone. Consistent with this view, aggregate demand—and in particular private consumption—contracted in France in the first quarter of 2022.

Within the euro area, it is our growing trade deficit—driven in particular by the rising energy bill—that allows us to “pay” for this energy cost. If oil-exporting countries were to purchase more goods from France (and other energy-importing countries)—for example, aircraft or military equipment—then the higher (nominal) cost of energy could be offset by increased exports, helping to finance the energy bill and support demand. Unfortunately, this is not the case, and rising energy prices are currently translating into an ever-larger trade deficit. Should this be a concern, and if so, what should be done? In the medium to long term, one solution—consistent with the need for ecological and energy transition—is to reduce dependence on hydrocarbons. In the short term, the choice is between pursuing restrictive policies that compress domestic demand and imports, leading to a lower standard of living, or maintaining domestic demand (as in the “whatever it takes” approach), which leaves open the question of how to finance the external deficit.

Monetary policy, which is supposed to act on demand even as demand is already being negatively affected, does not appear well suited to addressing this type of imported inflation shock. Monetary tightening can indeed help limit inflationary pressures, and it also operates through the exchange rate channel, as an appreciation of the domestic currency “exports” inflation abroad. For example, the Fed’s rate hikes led to a depreciation of the euro against the dollar of around 10%, to about $1.03, compared with around $1.13 before the war in Ukraine, which likely contributed to exporting inflation. Following the European Central Bank’s announcements of rate increases in July 2022, the euro seemed to have limited its depreciation to around 5% in early June ($1.08). As of June 30, 2022, the euro had fallen back to $1.04. In any case, “competitive disinflation” (echoing the 1980s and mirroring “competitive devaluation”) is ultimately a zero-sum game.

One argument in favor of monetary tightening is the idea that inflation should not be validated, for fear of triggering an inflationary spiral, particularly through a wage–price loop. This argument has been widely heard since inflation returned: to avoid setting off such a loop, some suggest not increasing nominal wages, in order to prevent so-called “second-round effects.” But is this not, at best, premature? For now, inflation is not wage-driven: real wages are falling rapidly, and the priority does not seem to be curbing a wage–price spiral that does not currently exist—at least in Europe. The experience of the 1970s may have led to excessive caution regarding such dynamics, which appear less relevant today given the widespread de-indexation of wages from inflation and the rarity of automatic indexation mechanisms.

Rather than focusing on demand control—particularly through restrictive monetary policies—it seems preferable to implement public policies that support supply in sectors under strain, enabling both the development of alternative energy sources and the expansion of export capacity. In a sense, this amounts to an (indirect) policy of “demand through supply.”

A new monetary environment

Even if monetary tightening is far from obvious in the current context, it is underway and appears set to continue—and even intensify. For now, the increase in nominal interest rates remains well below that of inflation, so that ex post real interest rates (nominal rates minus inflation) are declining. In this context, financial conditions should, according to standard economic theory, be more accommodative: strongly negative real interest rates are supposed to stimulate both consumption and private investment. This reasoning must, however, be qualified by considering the evolution of ex ante real rates—that is, the difference between nominal rates and expected inflation—which are more relevant determinants. It is possible that rising nominal rates help contain inflation expectations, so that ex ante real interest rates become positive. In that case, current conditions would still be highly accommodative, and a faster increase in interest rates (in theory, in line with inflation) would be feasible. But the same argument can also be used to justify a more rapid increase in interest rates, both because monetary conditions remain very accommodative and because only a substantial tightening may anchor inflation expectations at a low and stable level. That said, inflation expectations are difficult to measure, and their role in central bank decision-making remains debated (Tarullo 2017).

In reality, current financial conditions may be less favorable for the economy, even though real interest rates are lower, for three often overlooked reasons. First, fiscal rules—such as the Maastricht criteria (currently suspended)—are defined in terms of limits on the overall deficit, which includes both the primary deficit and interest payments on public debt. When nominal interest rates rise, the interest burden increases, reducing the room for maneuver on the primary balance and forcing either higher taxes or lower public spending—in short, a more restrictive fiscal policy that may weigh on growth. Yet this largely reflects an accounting artifact. What matters for debt sustainability is the real interest rate, not the nominal one. When inflation rises, public debt (denominated in euros and largely non-indexed—about 90% in France) becomes less burdensome. While higher interest payments appear as additional expenditure, the reduction in the real value of debt due to inflation is not recorded anywhere in national accounts. In simple terms, inflation generates a transfer from creditors to sovereign borrowers, as debt is repaid in depreciated currency. For this reason, if fiscal rules are deemed useful, they should arguably focus on the primary deficit rather than the overall deficit.

Second, persistently higher inflation mechanically tightens credit constraints for households seeking to buy property. These constraints are based on current income, of which only a fraction (currently about 35%) may be used to service a mortgage. When inflation rises, wage inflation also increases (though not necessarily to the same extent), so that current income represents a shrinking share of average income over the life of the loan. For a given real interest rate, higher inflation and higher nominal rates therefore make regulatory borrowing constraints more binding.

Third, rising nominal rates can have recessionary effects in countries where mortgage loans are predominantly at variable rates. France is relatively protected in this respect compared with many of its European partners, as only about 2% of new mortgages fall into this category (although this was not always the case: in 2005, just before the 2007–09 financial crisis, 35% of new mortgages were variable-rate). By contrast, this share is close to 100% in Poland, over 80% in Austria, and around 40% in Spain. This high degree of heterogeneity poses a risk within the euro area, as the effects of monetary policy are much stronger—and more immediate, particularly on borrowers’ disposable income—in some countries than in others, potentially leading to divergent interests regarding the conduct of monetary policy.

Indexation: a complex and incomplete form of protection

To summarize the above, imported inflation imposes a burden at the aggregate level that the government can either absorb (through a contraction in demand) or finance (by accepting an external deficit): this is the long-standing dilemma between adjustment and financing, the latter potentially implying an intertemporal or intergenerational transfer of the burden, as with any form of debt. Beyond this macroeconomic perspective, however, rising energy and food prices—as well as increases in other prices—also have differentiated impacts across economic agents. The redistributive effects therefore deserve close attention, and this is largely what underlies the debate on purchasing power: the stakeholders in this debate are not thinking in terms of an aggregate collective burden, but rather in terms of the effects on their own purchasing power. This, beyond the sharing of any aggregate burden, is a fundamentally different issue.

The distribution of losses in purchasing power raises the issue of indexation, which determines how the burden is shared between workers and shareholders, the public and private sectors (e.g. the public sector wage index), the state and taxpayers (through the indexation of income tax brackets), and so on. Indexation shapes both the allocation of an aggregate loss of purchasing power and the way inflation affects different social groups. Yet the choice of the type and extent of indexation is, on the one hand, deeply political—and is currently at the heart of political debates in the National Assembly—and, on the other hand, difficult to fully grasp due to two main obstacles: insufficient data and the complexity of the mechanisms involved.

Wage indexation, for example, appears to have an immediate effect on how the costs of inflation are shared between wages and profits. But if firms are also able to pass higher costs on to consumers, their profits may remain protected. Indexing public sector wages—through the value of the index point, for instance—determines how the burden is shared between public employees and current or future taxpayers, but this assumes that such increases are not financed through a sustained rise in public debt, which recent history suggests is unlikely. The rent reference index (IRL), meanwhile, is linked to inflation and therefore depends on oil and gas prices, which raises concerns insofar as tenants may bear energy price increases twice: once through utility charges and again through higher rents. For this reason, Hippolyte Dalbis has proposed excluding energy prices from the IRL formula—but this would effectively lead to under-indexation relative to construction costs, potentially resulting in reduced construction, housing shortages, or a segmented market between new and existing housing, with insider–outsider effects similar to those observed in Sweden. Rent controls during leases may also discourage tenant mobility. As these examples illustrate, determining rent indexation and how the burden is shared between landlords and tenants is far from straightforward in an inflationary context.

According to recent government announcements, the public sector wage index point is set to be increased by 3.5% in July. At the same time, basic pensions will be raised by 4% in July, following a 1% increase in January, bringing the total increase to around 5%. This raises the question of whether it is appropriate to fully preserve retirees’ purchasing power in a context where purchasing power losses must be shared. According to INSEE, the standard of living of retirees exceeded that of the working population on average as early as 2015. More generally, unless public resources are used to absorb the costs, protecting one group from inflation through indexation (workers, landlords, motorway concessionaires, or debtors) necessarily exposes another group, which then bears the inflationary shock (motorists, tenants, shareholders, creditors). In this sense, indexation is fundamentally a political choice.

A closer look at indexation mechanisms also highlights the limits of historical comparisons and the risks of applying analytical frameworks developed in different contexts. Consider, for example, the frequent comparison between the current period and the stagflation of the 1970s, marked by oil shocks. While the two periods share some similarities, the comparison is overly simplistic. We have already discussed the debate over the “wage–price spiral,” which in the 1970s was largely driven by widespread indexation and the practice of negotiating wages in line with inflation—practices that have largely disappeared today. Wage indexation was far more prevalent in the 1970s than it is now, and many wages were subsequently de-indexed in response to the oil shocks. The share of fossil energy in both final consumption and intermediate consumption was also higher at the time, partly because industry accounted for a larger share of the economy, but also because dependence on hydrocarbons has since declined. In addition, the Bretton Woods system had just collapsed, so the world was far less accustomed to flexible exchange rates, and central banks had not yet adopted the clear mandates they have today.

What should we think of the “energy price shield”?

Among the many government measures aimed at preserving households’ purchasing power, the “energy price shield”—which consists in capping gas and electricity prices—arguably deserves separate discussion. This policy tool is emblematic of the tensions that can arise between different forms of economic rationality. On the one hand, it helps protect purchasing power. On the other, it does not encourage a reduction in energy consumption or in imports of oil and gas—both of which are desirable for geopolitical reasons. It also raises questions in the context of the ecological transition, which aims to increase the price of carbon-intensive energy over the long term. In the current context, geopolitical objectives—penalizing Russia and reducing dependence on Russian oil and gas—align with environmental goals of reducing greenhouse gas emissions.

The energy price shield has therefore been criticized on several grounds. Most economists are generally skeptical of fuel price subsidies and of the price caps on electricity and gas (“tariff shield”) introduced and extended in urgency by the government. The reason is that higher prices send a signal of energy scarcity and costliness to consumers, encouraging them to reduce consumption. At the same time, higher prices also incentivize potential producers to increase supply. For this reason, economists often prefer more “targeted” support measures, which help (especially low-income) households without eliminating the price signal. Price caps thus fail to encourage short-term reductions in fossil fuel consumption, even though such reductions are desirable both morally (to avoid financing Putin’s war) and economically. In the longer term, they may also send the wrong signal, at a time when carbon prices are expected to rise. Should we trust the role of the “price signal”? In the 1970s, many analysts underestimated the long-term price elasticity of oil demand: in reality, consumption fell substantially following the oil shocks, before rising again after the counter-shocks of 1980 and 1986. This suggests that the price signal should not be ignored. However, why oppose it—as is often done—to the need for energy planning? Rising prices for carbon-intensive energy will not spontaneously create the alternatives consumers need to change behavior; without public policies and regulation, such alternatives may take a long time to emerge, thereby reinforcing declines in living standards. Moreover, the trajectory of energy price increases should be managed and not left to the vagaries of geopolitical developments. The organization of the energy transition should be deliberate, rather than relying on market mechanisms driven by constraints (whether through supply restrictions such as embargoes or through price signals) to force adaptation.

That said, the “shield” strategy also has some advantages. First, the economic cost of the war in Ukraine is in fact significant for the country, notably through higher energy prices. The energy price shield helps increase the political acceptability of this burden. One might nonetheless wish for price caps to be accompanied by measures encouraging reduced consumption and “sobriety” efforts—measures that have so far been largely absent in France, unlike in some other countries. Encouraging reduced consumption would arguably make more sense than attempting to punish Russia solely by restricting supply (through an embargo), which tends to raise prices as long as demand does not adjust and may even benefit Russia as long as the embargo is not fully implemented but merely anticipated.

Second, uncertainty about future commodity prices also weighs on energy consumers, who may hesitate to adjust their behavior or invest in response to price increases whose persistence they cannot gauge and may underestimate. More broadly, it is counterproductive in the long term to associate the energy transition with a decline in living standards, on the assumption that such hardship will generate the willingness to change behavior. One may also question whether the energy transition must necessarily be costly, which points to the value of greater planning and the use of a broader set of policy instruments. For example, when considering the trade-off between car or air travel and rail, should policymakers increase the cost of driving and flying—producing both substitution and income effects—or rather subsidize rail travel more heavily, achieving a similar substitution effect but with the opposite income effect?

Conceptual and statistical gaps

The current inflationary episode, much like in the 1970s, reveals the limits of macroeconomic thinking. Inflation remains an imperfectly understood phenomenon. This is also why both governments and central banks appear to be navigating by sight. Central banks are raising interest rates in a coordinated manner, without being fully certain that the effect on inflation will be sufficient. One can even observe a form of mimicry, often compelled: the European Central Bank is raising rates largely because the U.S. Federal Reserve is doing so; keeping rates near zero while the Federal Reserve increases them would lead to a depreciation of the euro, thereby intensifying inflationary pressures in the euro area. As discussed above, rising nominal interest rates in Europe are not well suited to the nature of the inflation shock we are experiencing and tend to constrain fiscal policy further, in part due to poorly designed fiscal rules.

The current episode also highlights the limitations of approaches that rely on sophisticated econometric analysis of macroeconomic time series in search of “natural laws” linking inflation to its determinants, without taking into account the institutional context—such as indexation mechanisms or energy pricing. Even if such “laws” exist, they clearly depend on the institutional framework, which itself reflects the balance of power between social groups at a given time. The lack of detailed statistical data on these institutional features severely limits our understanding of the mechanisms at play, as well as the validity of comparisons—both over time within a given country (for instance, comparing inflation dynamics today with those of the 1970s requires accounting for differences in wage indexation) and across countries.

As noted earlier, what primarily determines the evolution of inflation in response to rising oil prices is the detailed set of indexation mechanisms—automatic or otherwise—that are triggered by such shocks. Some prices are also automatically indexed to inflation (such as highway tolls, under concession contracts), as are certain taxes. To illustrate the complexity of the issue, property taxes in France are based on rental values that are updated annually—not according to the Consumer Price Index (CPI), which is used for most indexation in France (and published by INSEE), but according to the Harmonised Index of Consumer Prices (HICP) at the European level (published by Eurostat). Yet these indices do not evolve in exactly the same way (in June 2022, year-on-year inflation was 5.8% for the CPI versus 6.5% for the HICP). Similarly, income tax brackets are indexed to inflation, which, in the case of imported inflation, does not reflect income dynamics. This creates a dilemma between increasing tax revenues—by freezing tax brackets—and protecting taxpayers—by indexing them, since many would otherwise move into lower tax brackets or exit taxation altogether. While these mechanisms are relatively well understood in France, they are much less so in other countries, limiting the scope for meaningful international comparisons. Yet such detailed knowledge would be necessary to properly assess the economic effects of rising inflation across countries.

Moreover, it is not only data on indexation that are lacking or incomplete. The statistical conventions underlying the construction of price indices—and therefore indexation—are themselves largely arbitrary, complicating analysis and making international comparisons even more difficult. For example, a fuel rebate will be reflected in the consumer price index if it applies to the entire population, but will instead be recorded as income if it excludes certain groups (such as higher-income households). Yet the effect on the purchasing power of lower-income households is the same in both cases. Once again, the limitations of the statistical framework constrain our ability to analyze the situation—and therefore to act. If inflation persists, or if similar episodes become more frequent, it will be necessary to develop statistical tools better suited to such inflationary environments.

Conclusion

Protecting the purchasing power of French households is a priority in the face of an imported inflation shock whose analysis remains incomplete, and whose complex effects challenge both traditional economic frameworks and the available statistical data. So far, purchasing power has been broadly preserved through costly and unsustainable price controls, from which it may prove difficult to exit if the crisis persists. In this uncertain context—where the likelihood of a further worsening of the energy crisis later in the year is high—reconciling short-term constraints with the long-term imperatives of the energy transition is a formidable challenge. The inherently political nature of purchasing power protection, the persistent tendency to address political issues through technical approaches, and the lack of adequate knowledge and data all point toward a chaotic trajectory of ad hoc adjustments. This is precisely what “ecological planning” must strive to change.