Economic Policies to Combat Inflation in Europe

inflation

purchasing power

Europe

Although it had long seemed to have vanished from the European continent, inflation returned with force: annual inflation in the euro area reached 7% in April 2023, after peaking at 10.6% in October 2022.

Since then, combating inflation has become a central priority of economic policy, prompting European governments to deploy an unprecedented array of instruments. Price shields, reduced VAT rates, caps on gas prices for electricity generation, rent freezes, subsidized monthly transport passes, fuel rebates, tax exemptions on profit-sharing bonuses—not to mention the European Central Bank’s interest rate hikes: the list of measures adopted to fight inflation since the outbreak of the war in Ukraine in February 2022 reads almost like a catalogue à la Prévert.

This chapter sets out to survey these policies across Europe—whether aimed at external or internal sources of inflation—and to examine the underlying logic that has guided their design.

Where does inflation come from?

The war in Ukraine, the post-pandemic recovery, expansionary monetary and fiscal policies—there is no shortage of explanations offered to account for today’s inflation. Yet the absence of a shared diagnosis is itself a first obstacle for economic policy: each interpretation implies a different set of policy prescriptions.

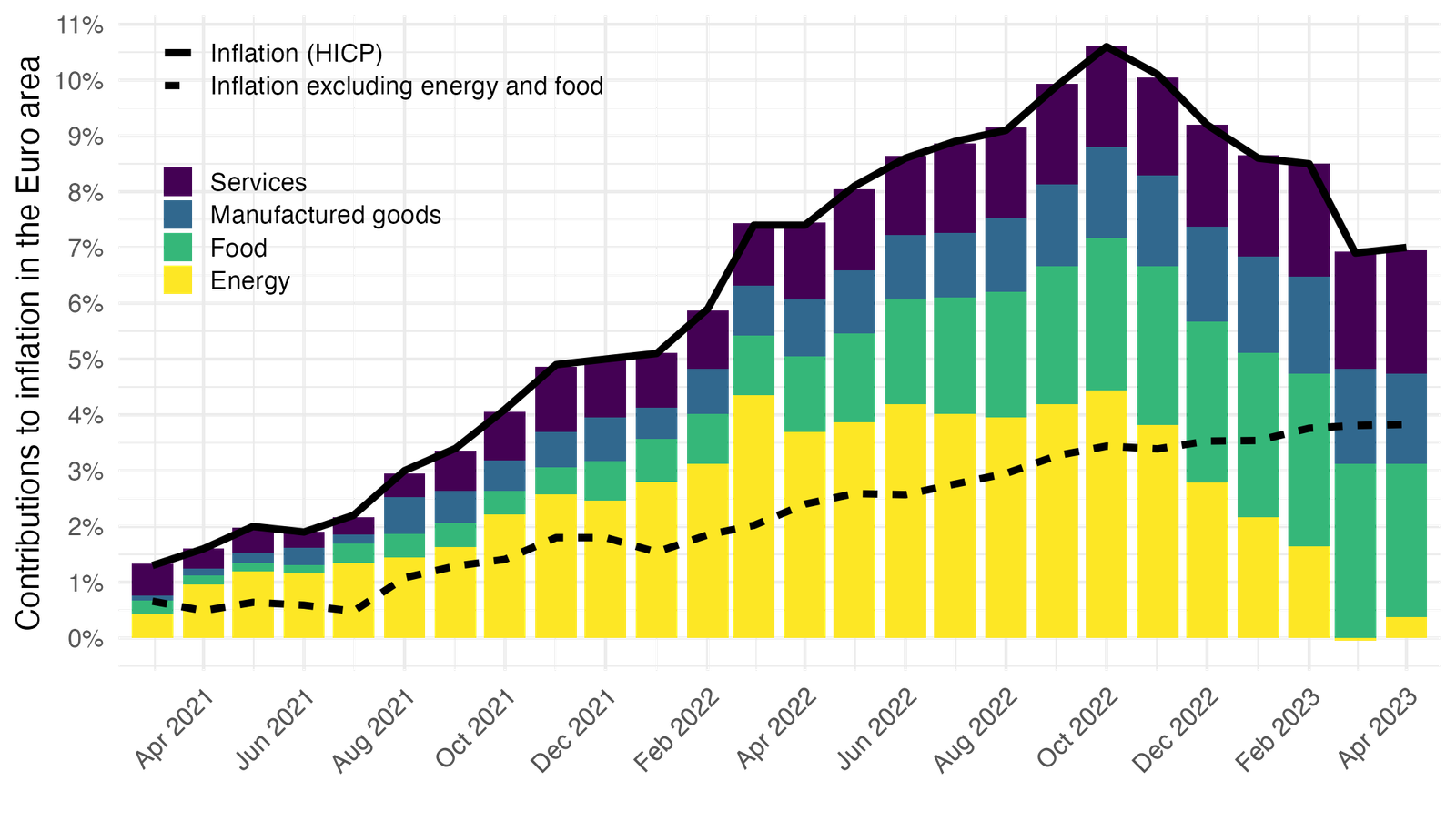

A closer look at the components of inflation, however, allows certain theories to be set aside. To begin with, contrary to accounts that attribute inflation solely to the growth of the money supply (in line with the quantity theory of money), it is undeniable that rising energy and food prices played a central role in the surge of euro-area inflation. As shown in Figure 1, at the peak in October 2022, the contribution of energy to inflation was around 4.4 percentage points, while food accounted for about 2.7 points—together contributing roughly 7.2 points. The contribution of all other components combined was therefore only around 3.4 points1.

By contrast, explanations that blame overly expansionary monetary policy or the fiscal “whatever it takes” response run into difficulties. Why, if these policies were decisive, did inflation not appear earlier—during the years of monetary expansion or at the height of the COVID-19 fiscal response—but only during the post-pandemic recovery? And why did inflation accelerate so sharply following the outbreak of the war in Ukraine, if not because of the obvious effect of the crisis on energy and food prices? Other factors, such as supply chain disruptions linked to China’s lockdowns, no doubt played a role, but their precise weight is hard to quantify given their unprecedented nature.

Box: External Inflation versus Internal Inflation

While economics textbooks generally define inflation as a “generalized increase in prices and wages,” in practice not all prices and wages rise in the same way. There are therefore at least as many inflationary phenomena as there are components of the price index. Nevertheless, for the purposes of analysis, it is useful to classify inflationary dynamics into two broad categories: external and internal.

On the one hand, what we propose to call external inflation corresponds to a deterioration in a country’s terms of trade, leading to higher import prices. This reduces the purchasing power of the country as a whole, which must buy goods whose prices have risen (for example, oil), thereby becoming poorer. It is precisely this type of inflation that has been observed in Europe since at least October 2021.

By contrast, internal inflation is of a different nature: it refers to increases in prices and wages that can generate both winners (sellers) and losers (buyers) within the same country, but whose aggregate effect on national purchasing power is, in a first approximation, neutral. It amounts to a decline in the value of money in terms of goods and services. Internal inflation can, for instance, be triggered by a sharp depreciation of a country’s exchange rate, as was the case in France or Italy during the “Trente Glorieuses.” These so-called “weak-currency” countries experienced significantly higher inflation than “strong-currency” countries such as Germany, Switzerland, or Japan. For some economists, the term “inflation” should in fact be reserved only for this latter case of internal inflation, since external inflation is nothing more than a rise in certain relative prices, not in all. However, the broader usage has become established in practice (Geerolf and Jacquet (2022)). The distinction between internal and external inflation is crucial, since the costs of external inflation are considerably greater than those of internal inflation. External inflation corresponds to a deterioration in the terms of trade, and thus to a genuine loss of aggregate purchasing power to be distributed across society. By contrast, the costs of internal inflation are much smaller, since there is no aggregate loss of national purchasing power. If such costs exist, they are of a second-order nature: in the New Keynesian framework, they stem from the dispersion of relative prices, which is a form of inefficiency. Yet their quantitative significance appears limited in practice, even under double-digit inflation (Nakamura et al. (2018)).2

The fight against this type of inflation is thus more a matter of political economy, aiming for instance to protect pensions and certain groups whose incomes or assets are not indexed, and who would otherwise suffer a decline in purchasing power. In the present euro area context, this objective of fighting inflation must be treated as a given, since it is enshrined in the treaties: one of the primary missions of the European Central Bank is to maintain price stability, with a mandate very similar to that of the former Bundesbank.

Beyond aggregate effects, the redistributive consequences of external inflation differ significantly from those of internal inflation. As we see today, external inflation weighs more heavily on poorer households (at least before indexation mechanisms are taken into account), whereas the distributive effects of internal inflation are more ambiguous. Internal inflation may, for example, benefit borrowers, or workers when it originates in wage dynamics. The common view that inflation disproportionately affects the poor is valid in the case of external inflation, but not in the case of internal inflation.

Finally, these two broad categories—external and internal inflation—do not exhaust the diversity of possible situations. Internal inflation can have multiple sources: it may arise initially from wage pressures, from profit dynamics, or from minimum wage indexation, which then propagate to other prices. Similarly, external inflation itself takes various forms, depending on whether it is driven primarily by oil, gas, electricity, or food prices, with distinct implications for both purchasing power and redistribution.

Reducing the Burden of the External Levy

One category of policies that directly addresses external inflation consists in reducing the external levy itself. These are without doubt the most effective, since they aim squarely at limiting the loss of purchasing power that must otherwise be distributed among economic agents. Yet such measures are rarely discussed by economists, who often take for granted that the external levy is exogenous to domestic economic policy—something outside the government’s control. In reality, however, a wide range of policies can mitigate its scope.

Energy policy is central in this regard. Within the European Union it remains largely the prerogative of member states, as confirmed by Article 194 of the Treaty on the Functioning of the European Union, which grants each country the right “to determine the conditions for exploiting its energy resources, its choice between different energy sources, and the general structure of its energy supply.” Not surprisingly, levels of energy inflation varied considerably3 across member states, reflecting differences in national energy mixes (Geerolf, Timbeau, and Allègre (2022)). Countries more dependent on imported gas and oil were naturally more exposed. As a result, strategies for curbing external inflation differed widely: while all Europeans had a shared interest in reducing overall energy consumption to lower prices, they also faced diverging incentives. Spain’s decision to cap gas prices in order to restrain electricity prices (the “Iberian mechanism”), for instance, drew criticism because it risked threatening Germany’s supply of gas by encouraging greater consumption in Spain. Similarly, the drive to secure alternative sources of liquefied natural gas (LNG) as a substitute for pipeline deliveries created competition among EU states as they sought to replace Russian supplies with cheaper alternatives.

Policies aimed at energy sobriety—encouraging households to consume less or firms to eliminate waste—proved effective, even if they revealed that untapped potential savings had long existed4. Such measures reduce inflation and the external levy in two ways: lower consumption softens the impact of any given price increase, and at the same time, it can ease pressure on prices themselves. Initiatives such as reducing highway speed limits or imposing stricter heating regulations could have formed part of this toolkit, though they were only partially deployed. On the supply side, reopening electricity generation capacity can also help by reducing import volumes and prices—though in Germany the reliance on coal plants carried an obvious ecological cost. Conversely, the weak availability of France’s nuclear fleet at the peak of electricity prices aggravated its energy bill, while the rapid effort to restart reactors significantly helped to bring it down. In this sense, the work carried out by Électricité de France (EDF), the Nuclear Safety Authority (ASN), and the Transmission System Operator (RTE) played a direct role in containing external inflation.

The fight against external inflation, however, was never purely economic; it was heavily shaped by geopolitical imperatives—most importantly, the determination to sanction Russia and support Ukraine’s war effort. In this context, limiting the scale of the external levy caused by sanctions serves two purposes at once: it curtails the terms-of-trade gains for the sanctioned economy, while also reducing the losses borne by the sanctioning economy. Some economists therefore argued for a full European embargo on Russian energy (oil and gas) in order to cut off Moscow’s financing.5 Yet such a move inevitably meant a dramatic rise in energy prices. Indeed, the announcement of the embargo, and its anticipation in markets through speculative stockpiling, triggered a sharp increase in prices. Paradoxically, this risked producing the opposite of the intended effect: bolstering Russia through higher export revenues while simultaneously enlarging the external levy for Europe. Rather than announcing supply cuts and relying on higher prices to suppress demand through price signals, a more judicious strategy might have been to organize reductions in demand in advance—through the kinds of energy-saving measures described above—which would have eased Europe’s energy bill without reinforcing Russia.

Containing the Rise in Energy Prices through Fiscal Policy

Even once measures to reduce the external levy have been implemented, households and firms may still face an excessive share of the burden. Shifting the increase in energy costs onto the state is another way of limiting energy-driven inflation—at the expense, however, of widening both the budget deficit and the external deficit. Such policies have been deployed to varying degrees across Europe: in France, through the costly bouclier tarifaire (tariff shield); in Spain, through cuts to VAT on energy prices. Obligations imposed on nationalized firms to sell energy below market prices, introduced in several European countries, also fall into this category. Subsidized monthly public transport passes, as seen in Germany, represent another way of easing household transport costs, and unlike fuel rebates they do not encourage carbon-intensive individual modes of transport (although Germany’s rail system is less carbon-efficient than France’s, given the higher share of fossil fuels in its electricity mix).

The major drawback of such policies is their potentially high fiscal cost. For this reason, measures such as tariff shields or fuel rebates have often been criticized as poorly targeted, benefiting too broad a population rather than focusing on those most in need. At the same time, studies have shown that the determinants of energy consumption are varied and not solely linked to income, making fine targeting difficult—especially under the pressure of urgency. Price-based measures do have one inherent advantage: they provide immediate relief precisely to those most exposed to the surge in energy costs. This applies both to fuel rebates and to VAT reductions on essential goods.

It is also important to stress that the rise in external inflation and in the external levy is not simply a supply shock raising firms’ production costs. It also functions as an aggregate demand shock, reducing household budgets and therefore demand. Policies to fight external inflation thus serve not only to contain inflation but also to mitigate the fall in aggregate demand and disposable income that inevitably accompanies food and energy shocks, which weigh disproportionately on households. Without such policies, household disposable income would be substantially reduced, forcing cutbacks in other consumption. On the one hand, this would compress imports and thereby dampen the trade deficit associated with the external levy. On the other hand, it would almost certainly generate higher unemployment and a larger budget deficit through Keynesian effects. In practice, these expansionary fiscal policies to combat external inflation have proven remarkably effective at reducing inflation—an unusual outcome, since fiscal expansion is typically expected to fuel inflation by boosting aggregate demand relative to supply.

From a microeconomic perspective, these policies have also faced criticism for weakening the “price signal.” By lowering the cost of energy, they fail to encourage conservation and thereby risk increasing both the energy bill and the external levy—working in the opposite direction from policies of energy sobriety. In this respect, Germany’s approach has often been cited as a model of prudence and sound economic management. The German scheme subsidized 80% of the previous year’s energy consumption, leaving the final 20% fully exposed to market prices. This preserved incentives to save energy at the margin while supporting household purchasing power and protecting firms’ operating capacity—effectively reconciling social protection with economic efficiency by maintaining intact incentives to economize on energy, thus significantly lowering the overall energy bill.

By contrast, tariff shields or cuts to indirect taxes on energy prices, as implemented in countries such as France, did little to encourage energy savings. Yet the German mechanism that preserved the price signal is hardly a perfect solution either. It tends to reward those who had not previously made energy-saving efforts, creating a form of time inconsistency: it rewards immediate reductions but, if repeated, risks discouraging households and firms from making savings in advance, in anticipation of future subsidies. For this reason, such schemes cannot be credibly implemented on a recurring basis without undermining voluntary energy conservation. In short, it is extremely difficult to design public policies that dominate all others. Each approach carries its own strengths and weaknesses, and the trade-offs between them are unavoidable.

Tackling the “Wage–Price Spiral”

Alongside policies aimed at external inflation, there are also measures targeting internal inflation. The two are not independent: one reason why countries such as France sought to curb external inflation as much as possible through public spending was precisely to limit the risk of a “wage–price spiral.” According to this theory, rising prices trigger higher wages (in a one-to-one relationship, known as “full indexation”), which in turn fuel further price increases. An alternative to shielding households from inflation through measures such as tariff caps would have been to provide them with larger direct transfers, as was done for example in Germany—measures that would not have appeared in the inflation statistics6. Fears of a wage–price spiral also led some governments to encourage one-off bonuses, such as France’s “Value-Sharing Bonus” (Prime de Partage de la Valeur), rather than permanent wage increases.

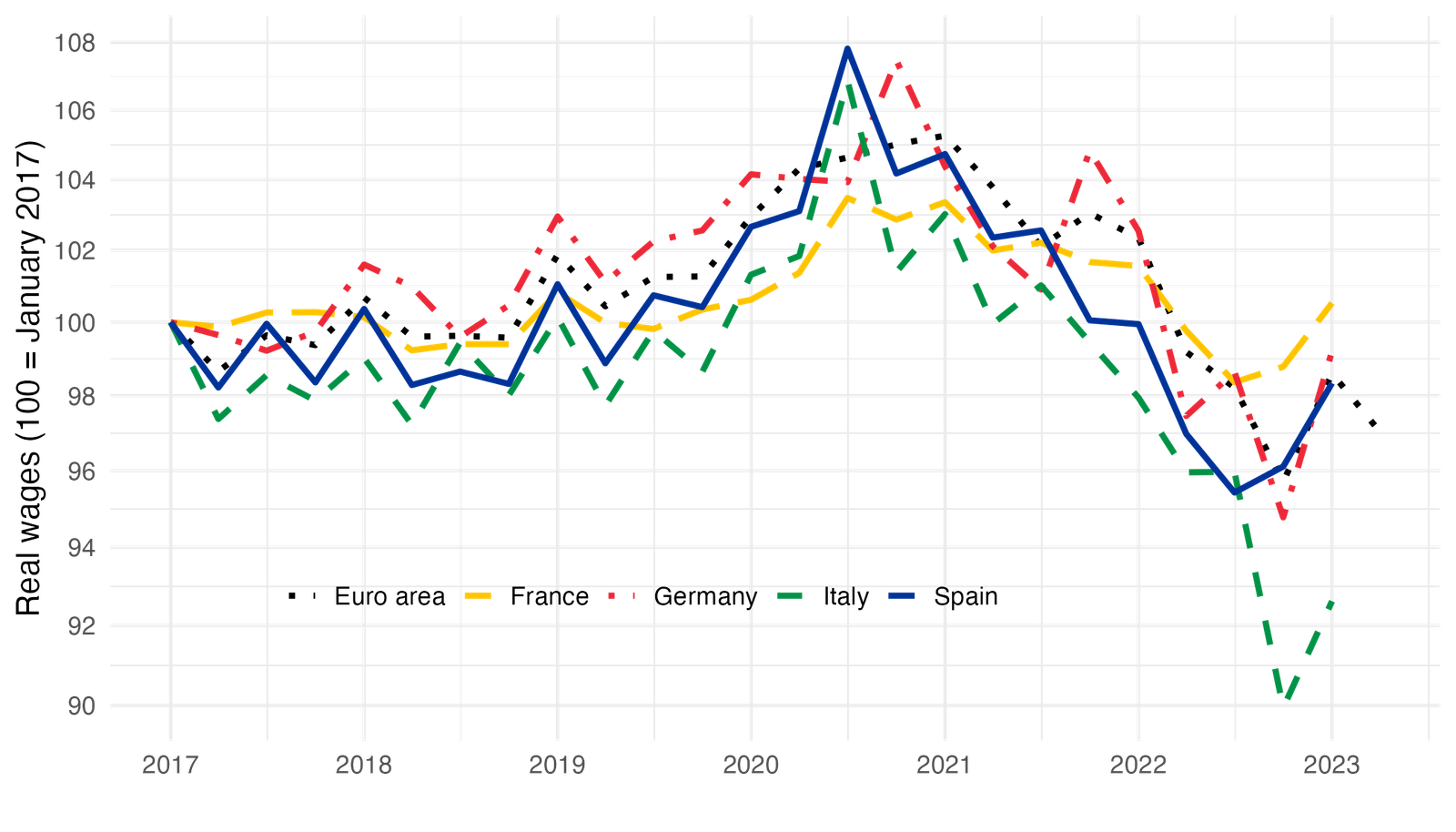

Yet there are good reasons to be skeptical of the wage–price spiral thesis. Empirically, across Europe nominal wage growth has been far below price inflation, resulting in declining real wages, as shown in Figure 2. In other words, there is little evidence so far of full indexation of wages to prices. If anything, nominal wages have tended to act as a stabilizing force, slowing the momentum of inflation rather than amplifying it.

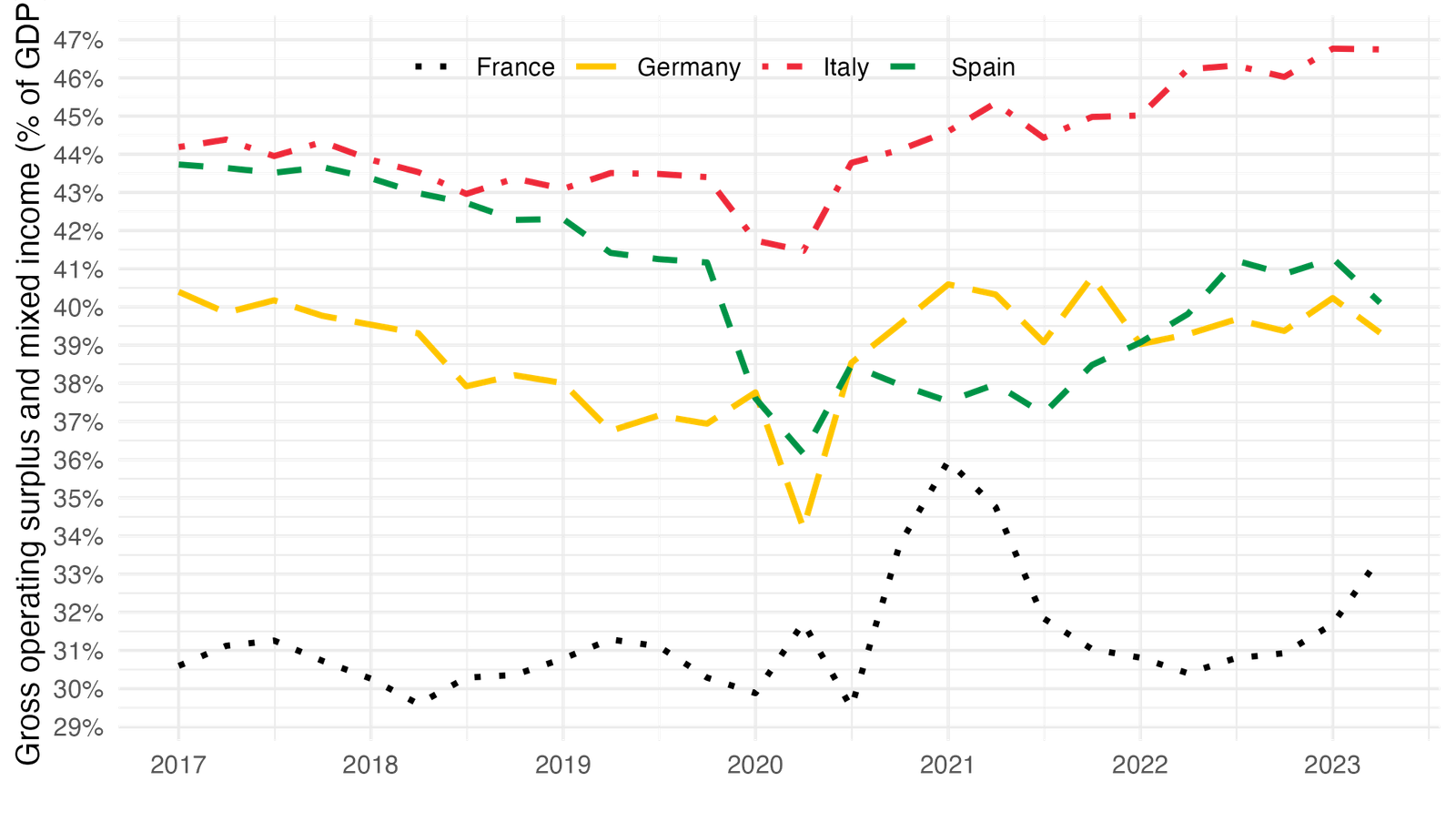

The debates around a “profit–price spiral” or even a “price–price spiral” suggest that profits have played a far greater role in driving inflation than wages. In many European countries, such as Spain and Italy, the profit share in value added (measured as gross operating surplus and mixed income) has in fact increased, as shown in Figure 3. The inflationary episode has therefore come at the expense of workers rather than to their benefit—an outcome that is rather unexpected in times of economic difficulty, and very different from the 1970s, when corporate margins eroded sharply. This has rekindled debates over an inflation dynamic not driven by wages but by distributional conflict among economic actors (Lorenzoni and Werning (2023)) - a question raised long ago during a previous inflationary episode (Rowthorn (1977)).

Guarding Against the “Unanchoring” of Inflation Expectations

Another key concern driving Europe’s forceful fight against inflation is the fear of a possible unanchoring of inflation expectations. Since the stagflation of the 1970s, expectations have been seen as central to the inflationary process. According to this view, inflation could become entrenched in Europe if economic agents began to anticipate higher rates of inflation and to incorporate them into their decisions. Once embedded, inflation would then be much more costly to reduce. This concern underpins the vigorous stance of central banks and their deliberate rhetoric, assuring the public that inflation will soon return to target—“in a timely manner.”7

Yet this fear rests on neither solid empirical nor theoretical foundations (Rudd (2022)). In practice, inflation expectations have limited predictive power for central banks; they have been most useful in retrospect, in explaining the stagflation episode of the 1970s (Tarullo (2017)). But that episode also coincided with a shift in the international monetary regime, with the collapse of the Bretton Woods system, which may itself explain the onset of stagflation following the dollar’s devaluation (Geerolf (2021)). Conversely, countries whose currencies appreciated most strongly at that time, such as Germany, experienced the lowest levels of inflation.

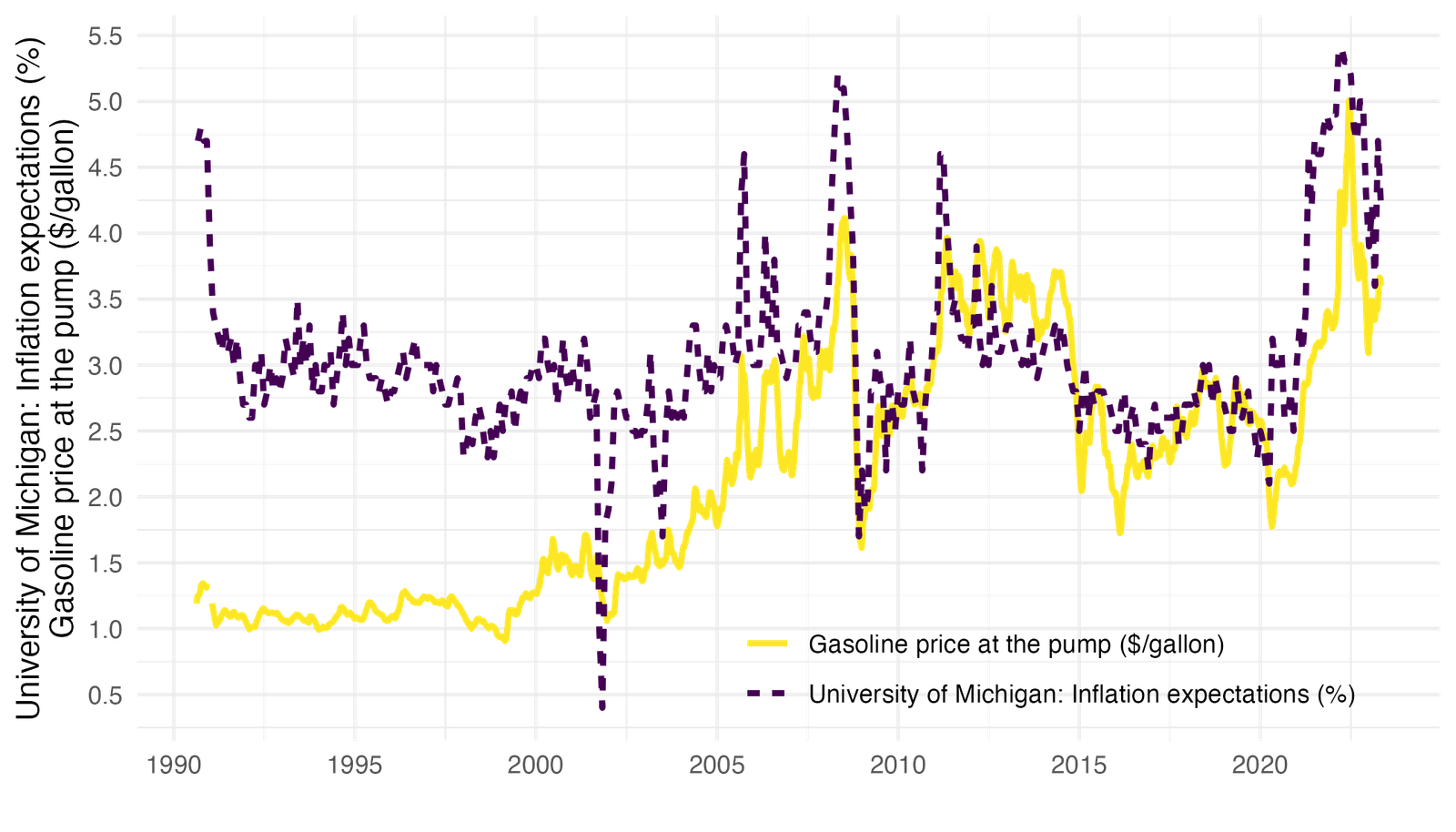

More broadly, microeconomic studies raise doubts about the extent to which inflation expectations actually shape the behavior of agents, including firms—many of which have little sense of average inflation at all (Coibion, Gorodnichenko, and Kumar (2018)). Likewise, households are often unaware of the central bank’s shifting targets (Coibion et al. (2023)). Empirically, it is striking that inflation expectations mostly track gasoline prices at the pump, as shown in Figure 4. This is perhaps unsurprising: these prices are highly visible to households and fluctuate significantly. But it raises the question of how much influence central bank actions can really have over expectations. Finally, as already noted, workers are struggling even to negotiate wage increases that compensate for past inflation. It is difficult to imagine how they might secure raises based on their subjective expectations of future inflation.

Raising Unemployment?

The stagflation of the 1970s not only convinced central bankers of the importance of inflation expectations; it also persuaded them that only a harsh policy of raising unemployment could curb inflation—taming both inflation itself, through the logic of the “Phillips curve,” and agents’ expectations of it. Paul Volcker is often celebrated for having defeated inflation in the early 1980s by deliberately engineering a sharp rise in unemployment, triggered by the Federal Reserve’s extremely restrictive monetary policy. In September 2022, Federal Reserve Chair Jerome Powell declared that he “needed higher unemployment.” He added: “To bring down inflation, we will need a period of below-trend growth and some softening in labor market conditions. (…) I wish there were a painless way to do that. There isn’t.” Since the onset of the current inflationary episode, the question has therefore been whether such a rise in unemployment will again be necessary to bring inflation down—or whether a “soft landing,” that is, a reduction in inflation without higher unemployment, might be possible.8

Yet as with inflation expectations, one may ask whether the right lessons from the Volcker era have really been learned. The United States also overcame inflation in the early 1980s by exporting it abroad through a very sharp appreciation of the dollar, a consequence of the Fed’s restrictive policy, which undermined U.S. competitiveness—particularly relative to Japan and Europe—and eventually led to the Plaza Accord. This is even more relevant for Europe today, where inflation has not been driven primarily by wages but by energy prices. In such circumstances, it is difficult to see how higher unemployment or slower growth could serve as an effective remedy.

Adjusting Indexation Mechanisms

Another tool for addressing internal inflation is to act on indexation. The widespread de-indexation of wages in most advanced economies around the late 1970s and early 1980s helped to prevent a potential wage–price spiral and to limit inflation. Today, indexation mechanisms still exist, particularly for minimum wages, which are indexed in many European countries, though the formulas and frequency vary. Beyond the minimum wage, institutional differences remain significant: in some countries collective bargaining takes place annually, while in others it occurs only every two years. The frequency of contractual negotiations more generally has an effect on inflation: this explains, for example, why food price increases occurred later in some countries such as France.

Indexation extends to other goods and services as well, such as rents in many countries (including France) or, more marginally, highway tolls in France. Here again, limiting indexation—for instance, capping rent increases at 3.5% per year in France—can help to curb internal inflation. But such measures also carry major distributional consequences, shifting the burden of inflation from one group to another (in this case, from tenants to landlords). All of these examples underscore the fundamentally political nature of debates over inflation and purchasing power. Beyond technical arguments among economists, these issues ultimately concern how the costs of inflation are distributed across society (Geerolf and Jacquet (2022)).

Bibliography

Bachmann, Ruediger, David Baqaee, Christian Bayer, Moritz Kuhn, Andreas Löschel, Benjamin Moll, Andreas Peichl, Karen Pittel, and Moritz Schularick. 2022. “What If? The Economic Effects for Germany of a Stop of Energy Imports from Russia.” 36. ifo Institute - Leibniz Institute for Economic Research at the University of Munich. https://econtribute.de/RePEc/ajk/ajkpbs/ECONtribute_PB_028_2022.pdf.

Coibion, Olivier, Yuriy Gorodnichenko, Edward S. Knotek, and Raphael Schoenle. 2023. “Average Inflation Targeting and Household Expectations.” Journal of Political Economy Macroeconomics 1 (2): 403–46. https://doi.org/10.1086/722962.

Coibion, Olivier, Yuriy Gorodnichenko, and Saten Kumar. 2018. “How Do Firms Form Their Expectations? New Survey Evidence.” American Economic Review 108 (9): 2671–2713. https://doi.org/10.1257/aer.20151299.

Geerolf, François. 2021. “La Courbe de Phillips n’est Pas Celle Que Vous Croyez.” La Lettre Du CEPII, no. 417 (April). https://www.cepii.fr/PDF_PUB/lettre/2021/let417.pdf.

———. 2022. “The ‘Baqaee-Farhi Approach’ and a Russian Gas Embargo.” Revue de l’OFCE 179 (4): 143–65. https://doi.org/10.3917/reof.179.0143.

———. 2023. “La Politique Économique En Europe Face à l’inflation.” Cahiers Français 432 (2): 64–73. https://doi.org/10.3917/cafr.432.0064.

Geerolf, François, and Pierre Jacquet. 2022. “Inflation Et Pouvoir d’achat : It’s the Politics, Stupid!” Relançons Le Débat Économique, June. https://lecercledeseconomistes.fr/articles/finance/inflation-et-pouvoir-dachat-its-the-politics-stupid/.

IEA. 2023. “Gas Market Report, Q1-2023.”

Lorenzoni, Guido, and Iván Werning. 2023. “Inflation Is Conflict.” Working {Paper}. Working Paper Series. National Bureau of Economic Research. https://doi.org/10.3386/w31099.

Nakamura, Emi, Jón Steinsson, Patrick Sun, and Daniel Villar. 2018. “The Elusive Costs of Inflation: Price Dispersion During the U.S. Great Inflation.” The Quarterly Journal of Economics 133 (4): 1933–80. https://doi.org/10.1093/qje/qjy017.

Rowthorn, R. E. 1977. “Conflict, Inflation and Money.” Cambridge Journal of Economics 1 (3): 215–39. https://www.jstor.org/stable/23596632.

Rudd, Jeremy B. 2022. “Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?).” Review of Keynesian Economics 10 (1): 25–45. https://www.federalreserve.gov/econres/feds/files/2021062pap.pdf.

Tarullo, Daniel K. 2017. “Monetary Policy Without a Working Theory of Inflation.” Brookings. https://www.brookings.edu/research/monetary-policy-without-a-working-theory-of-inflation/.

Footnotes

Underlying inflation, which excludes prices subject to government intervention (electricity, gas, tobacco, etc.) as well as products with volatile prices (oil products, fresh produce, dairy, meat, etc.), was in fact 5%, rather than 3.4%. This difference stems from a technical issue in the construction of price indices, related to the non-additivity of inflation rates.↩︎

It is interesting to observe the reactions elicited by this article when Emi Nakamura presented it at the European Central Bank’s annual research conference. One participant voiced skepticism by invoking the historically traumatic episode of hyperinflation in Germany.↩︎

The heterogeneity of energy inflation also reflected methodological differences in statistical measurement. For example, the Netherlands only includes energy prices from new contracts in its inflation index, which results in systematically different dynamics (Geerolf (2023)).↩︎

Economists are generally reluctant to make this assumption, since it implies that agents’ prior behavior was suboptimal. Yet empirical evidence—both for households and for firms—shows that such energy savings are indeed possible (IEA (2023)).↩︎

A widely discussed study (Bachmann et al. (2022)) in Germany, for example, considered a Russian gas embargo that would drive a fourteen-fold increase in energy prices in order to induce a 10% reduction in consumption, and a thirty-five-fold increase in gas prices (from €20/MWh to €700/MWh) to achieve a 30% decline in natural gas consumption (Geerolf (2022)).↩︎

The criterion for determining whether household support appears in measured inflation or in household nominal income depends on its universality and on whether it is directly linked to a purchase—criteria that vary across national statistical institutes. The division between inflation and nominal income is therefore to some extent arbitrary (Geerolf (2023)).↩︎

The phrase ‘in a timely manner’ is frequently used by ECB officials, including Christine Lagarde on March 22, 2023.↩︎

According to the latest forecasts by the OFCE (see Chapter 1) and the IMF, the euro area is expected to avoid a recession in 2023.↩︎